Key benefits

- Deep clearing liquidity pools

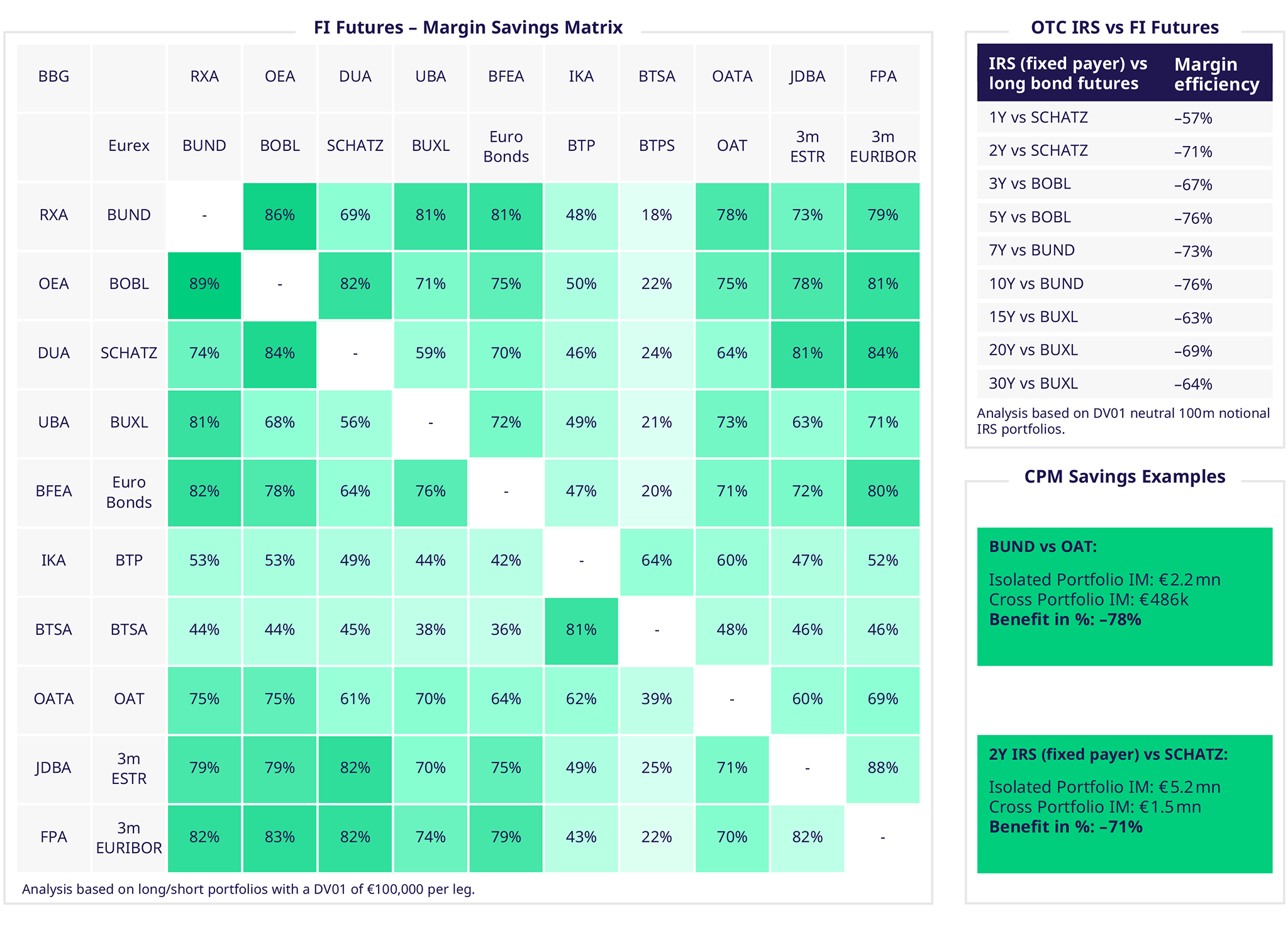

- Cross-product margining along the complete Euro yield curve without any maturity constraints, allowing for up to 70% initial margin savings

- Wide IRD product coverage, including FRA, IRS, and OIS

- Broad suite of listed interest rate derivatives, both short-term and long-term, including Euro-EU Bond Futures, futures on the Euro STR, futures and options on the EURIBOR and on the German Bund, Bobl, Schatz and Buxl

- Higher capital efficiencies: greater netting effects between listed and OTC positions

- Single cross-product collateral management solution

Calculation example

Our cross-product margining (CPM) algorithm captures the offsetting relationship of holding long and short positions in correlated fixed income asset classes. The figures below show the margin savings achievable within the fixed income futures universe and between OTC IRS and fixed income futures, where strategies are always offsetting in DV01 terms.

The algorithm recognizes the DV01-neutrality of these trades and calculates an amount of initial margin reflective of the reduced risk embedded in the offsetting nature of these trades. These capital charge reductions are not exclusive to such structured trades but are also seen in real-life portfolios of hundreds of long and short positions across OTC swaps and listed fixed income futures.

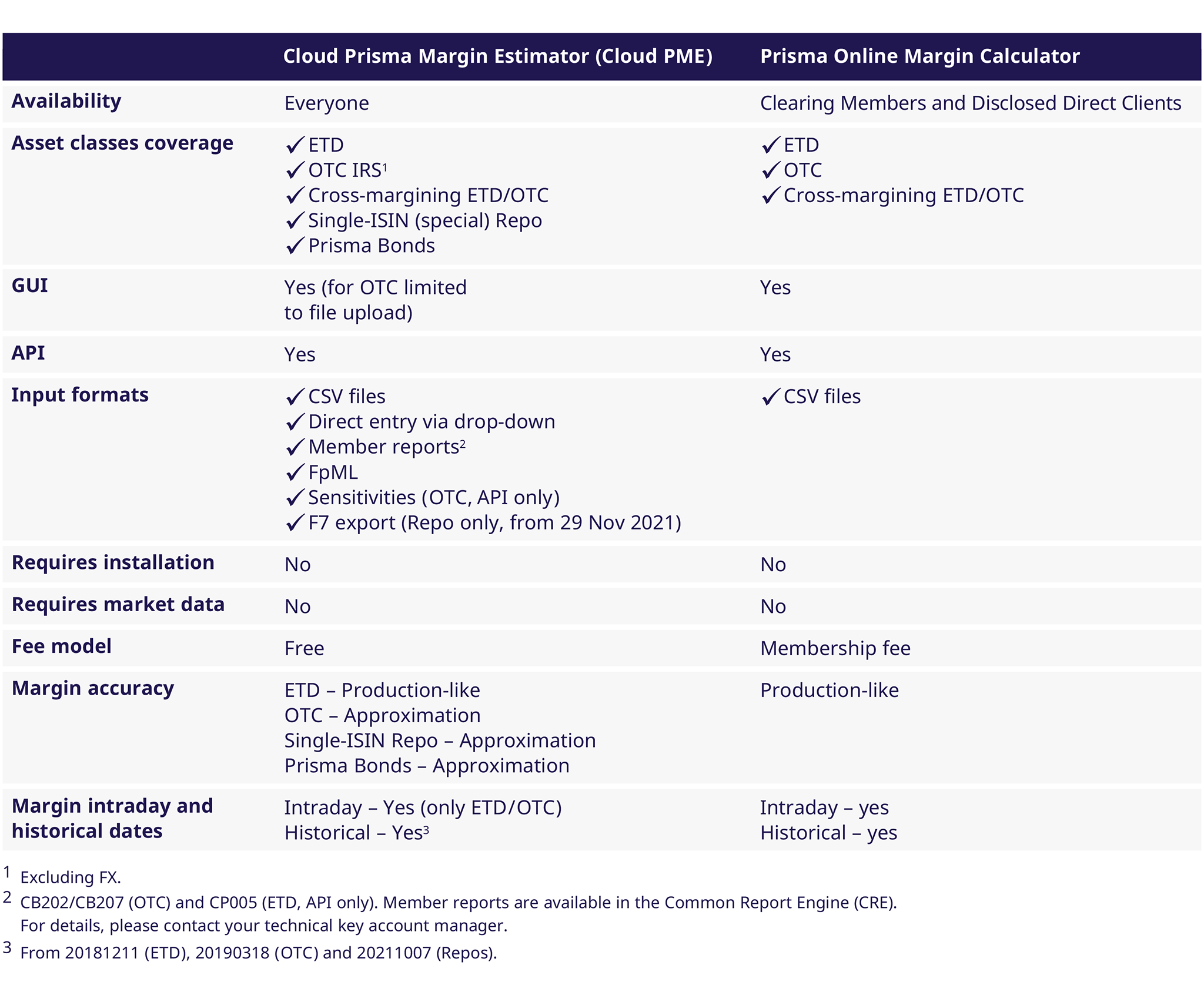

Prisma Margin Calculators

At Eurex Clearing, we understand that sophisticated margin replication and simulation is essential for our members and their clients. To this end, we offer several tools to calculate and simulate margin requirements within the Eurex Clearing Prisma framework, with each tool designed for a different use case:

- The Prisma Online Margin Calculator is a browser-based tool for members, running on Eurex Clearing’s production and simulation environments.

- The Cloud Prisma Margin Estimator (Cloud PME) is a cloud-based calculator accessible by GUI and API.

Our margin calculators can be used intraday via API to indicate the potential savings from clearing both fixed income listed and OTC derivatives at Eurex.