Jun 09, 2026

Eurex

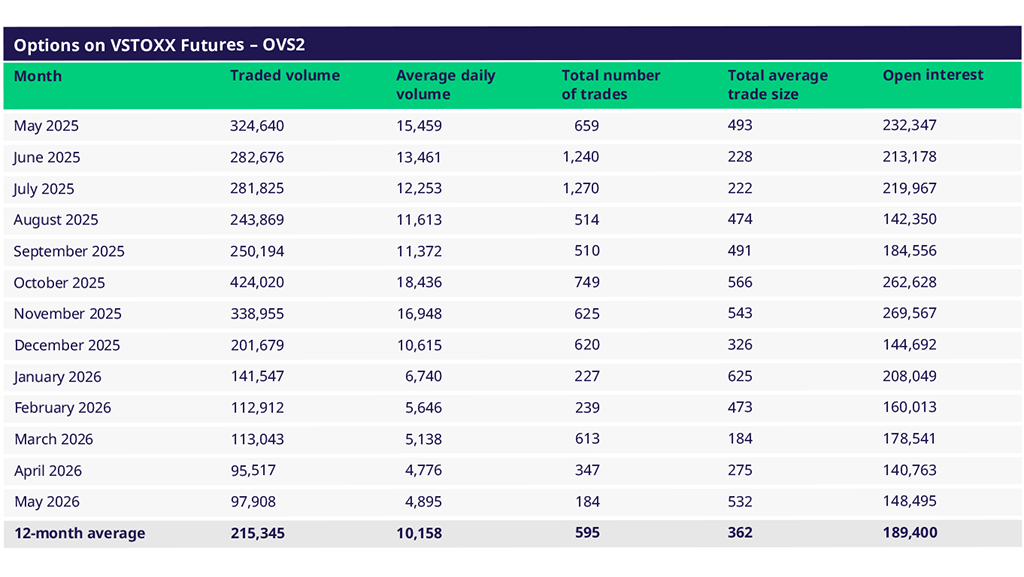

Focus on VSTOXX® Derivatives: May 2026 Recap

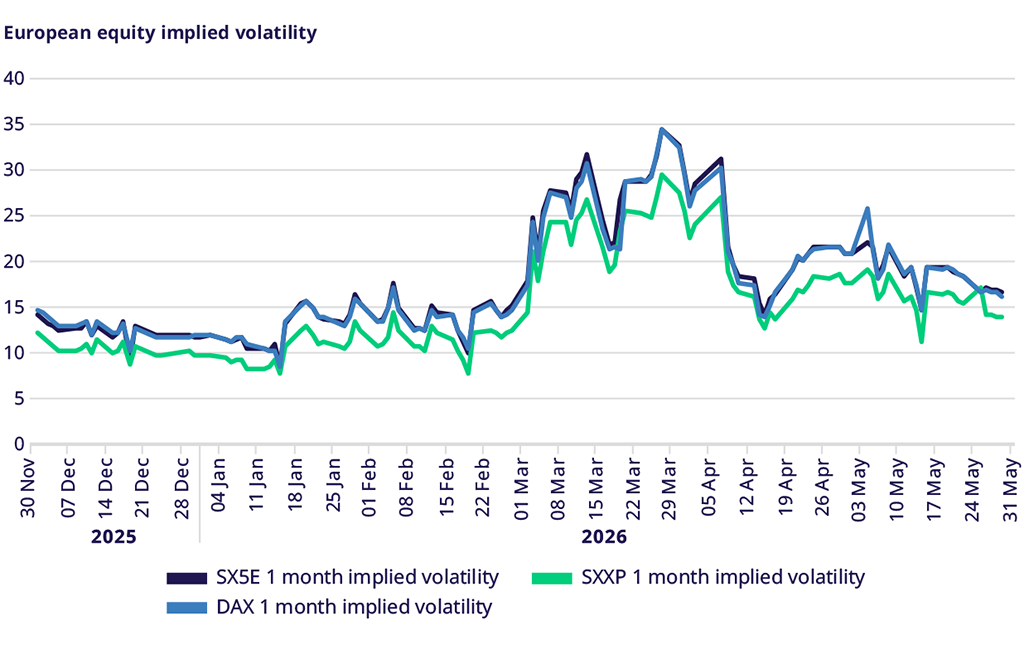

European markets were much stronger in May, following strong performance in April. The EURO STOXX 50® Index was up 2.87%, the STOXX® Europe 600 Index was up 2.41%, and the DAX® was up 3.34%. The All-Country World Index was up 4.98% as global stock indices continued to achieve a strong second quarter.

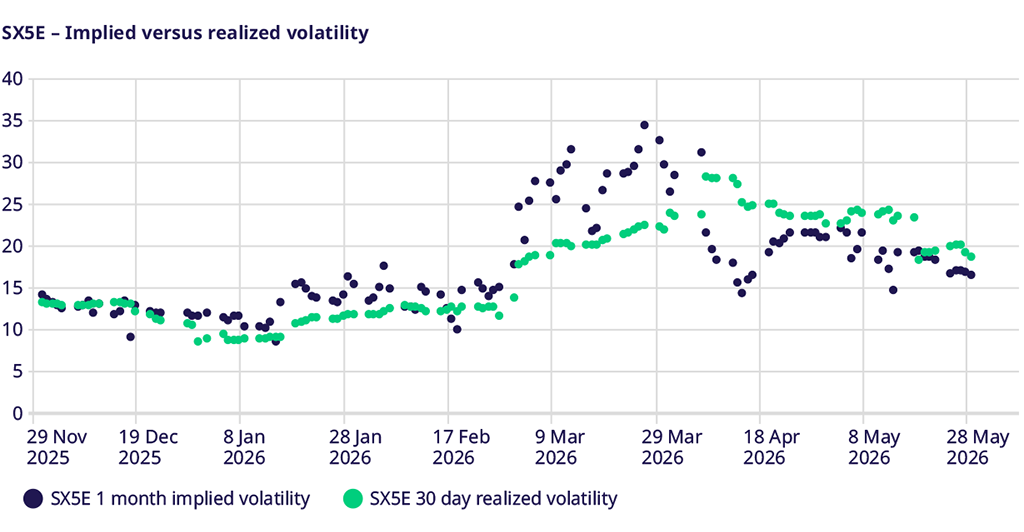

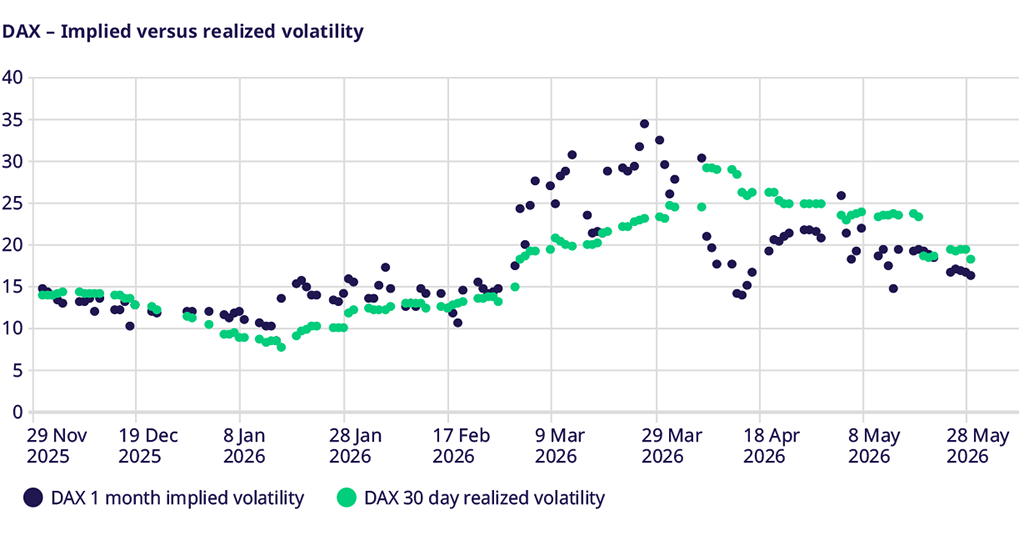

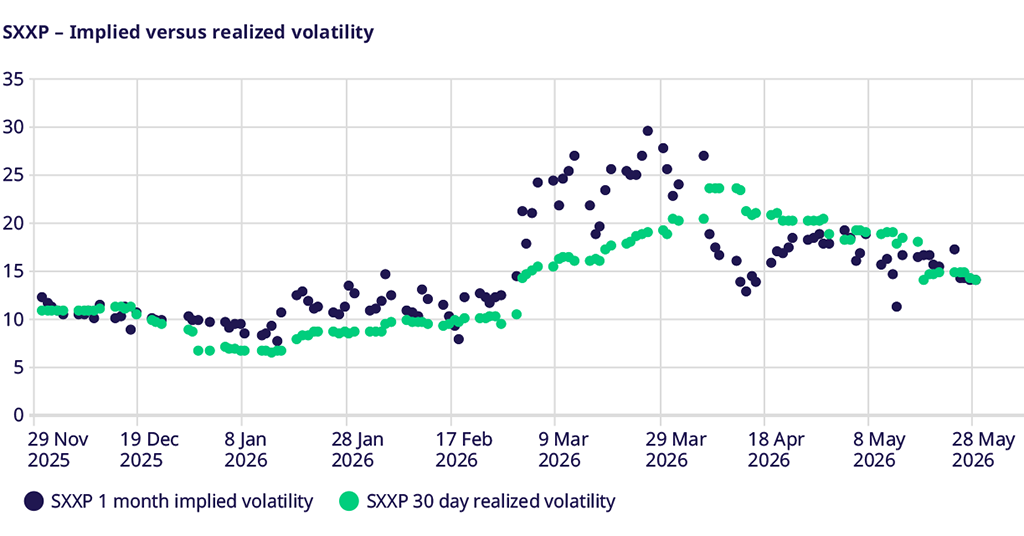

With markets rising rapidly, implied volatility finally eased, with declines across the board for European index volatility. The EURO STOXX 50® implied volatility fell from 20.95 to 16.53, the STOXX® Europe 600 implied volatility fell from 17.73 to 13.95, and the DAX® implied volatility fell from 20.75 to 16.16.

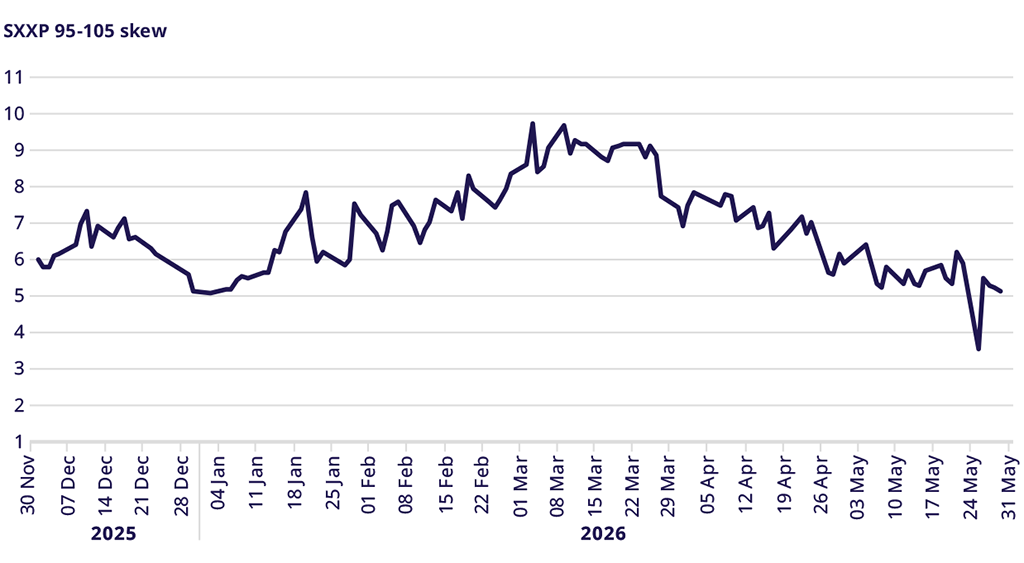

Skew declined modestly from 5.89 to 5.12 volatility points, remaining below the highs of almost 10 volatility points seen in early March and the six-month mean of 6.75 volatility points.

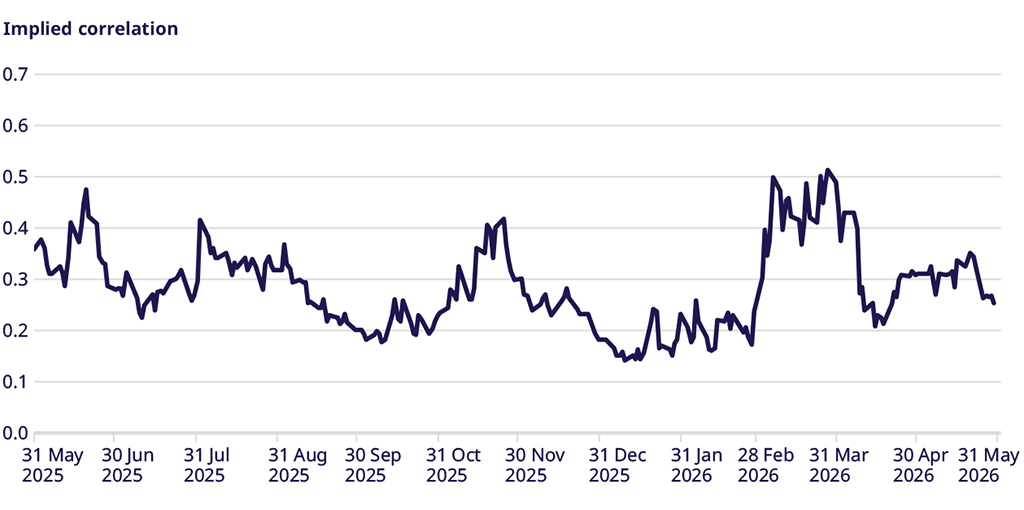

Implied correlation also declined from 0.3114 to 0.2527, remaining below its long-run average of 0.2891, with greater focus on single-stock idiosyncratic events.

Equity Index Volatility

While equity implied volatility remained relatively firm in April despite higher index prices, it finally eased in May on the back of continued market strength. Implied volatility fell by approximately 4 volatility points in each of the major index markets, and all now sit just below the six-month mean implied volatility. Notably, EURO STOXX 50 (SX5E) implied volatility at 16.53 is two volatility points below the trailing 30-day realized volatility, as is DAX implied volatility at 16.16. STOXX Europe 600 implied volatility of 13.95 is in line with trailing realized volatility. The compression of the volatility risk premium suggests that traders expect a continued moderation of market volatility.

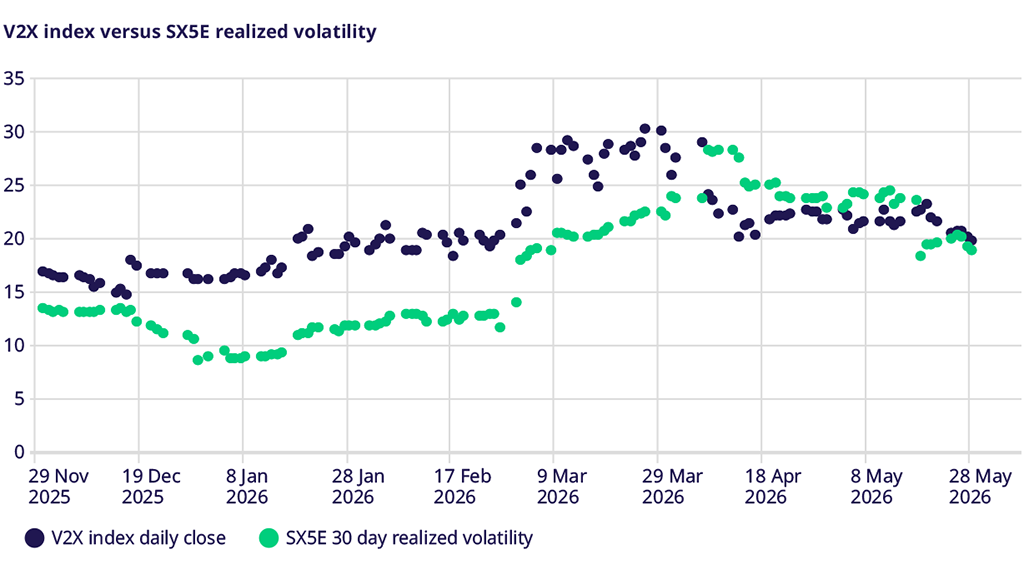

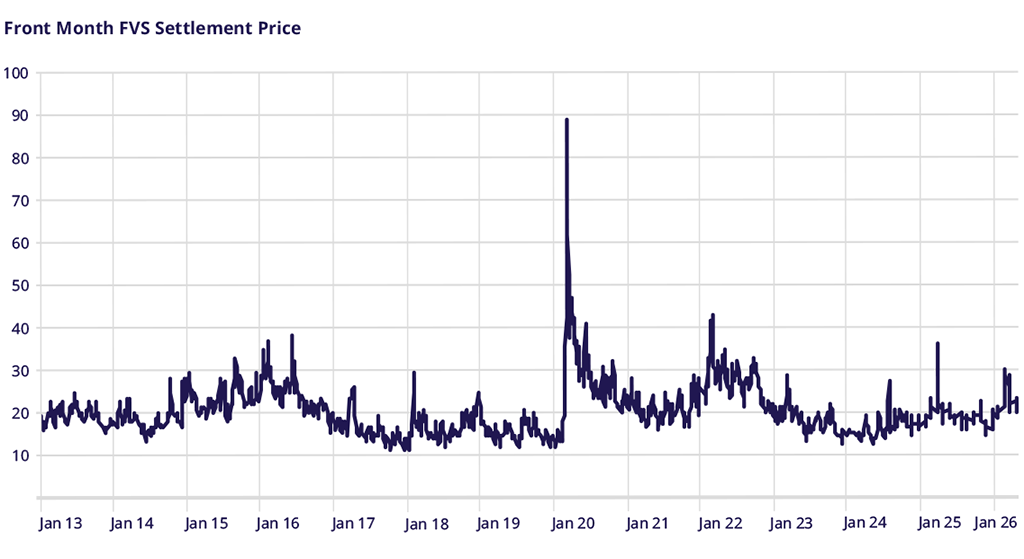

VSTOXX Index Performance

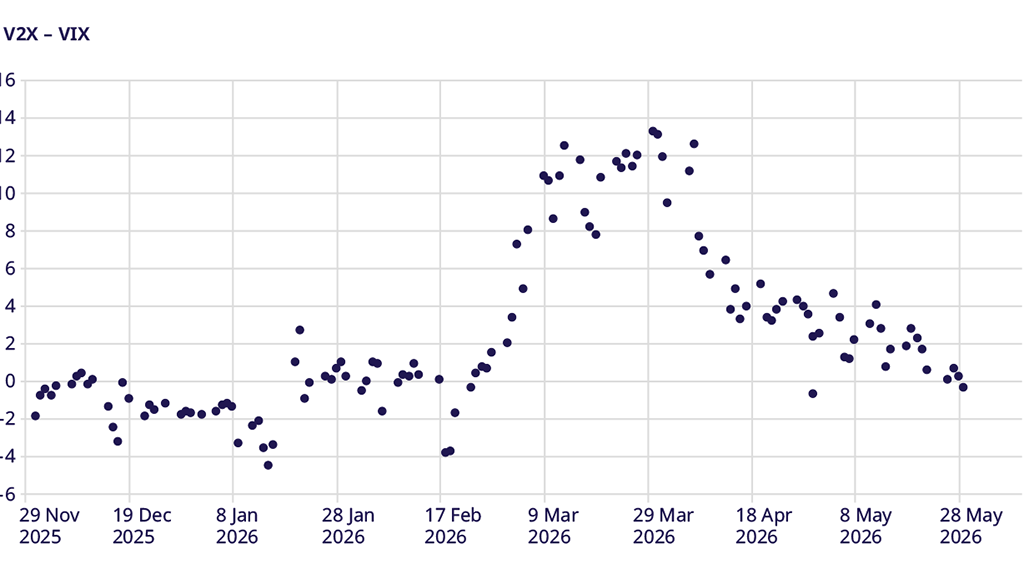

Similar to the index implied volatility markets, a continued expectation of moderating risk is also seen in the VSTOXX® market. The V2X Index level of 19.7 is only one volatility point above the EURO STOXX 50 (SX5E) 30-day realized volatility of 18.7. In addition, the spread between V2X and VIX closed the month at –0.66, with VIX closing slightly higher at 20.36. European risk markets appear to anticipate lower risk on the horizon.

STOXX Europe 600 Index Skew

Perhaps in a sign that investors continued unwinding portfolio hedges, STOXX Europe 600 Index skew fell from 5.89 to 5.12 volatility points, below the six-month average of 6.75 volatility points and well below the 9.78 volatility points seen at the start of the Middle East conflict in early March. There appears to be little desire to lock in recent equity gains by demanding downside index protection.

Correlation

Even though earnings season is wrapping up, the fall in implied correlation from 0.3114 to 0.2527, below the long-run mean of 0.29, suggests that traders are more focused on single-stock than index-level risks in the options market.

Trade the European volatility benchmark

Explore this year's macro events and find an overview of dates.

VSTOXX 101: Understanding Europe’s Volatility Benchmark

Discover the latest STOXX whitepaper today to learn more about the VSTOXX® core methodology, historical performance analysis, and more.

For more information, please visit the website or contact: